Instalments

The feature allows the cardholder to convert credit card transactions into instalments. In practice, this means transactions can be divided into smaller equal payments over a certain period which allows the cardholder to finance larger purchases.

Use Cases for Revolving Credit Instalments

- Annual Software License Fee: A company has a yearly software license fee that has a lower price if paid in one portion. Instead, the company chooses to pay in one portion, and then split the transaction into three instalments, allowing for easier payment management over time.

- Extended Credit Balance Repayment: Cardholders, whether private individuals or corporate entities require additional time to repay their credit balance. They have the option to convert a portion of the credit balance into instalments, granting them more flexibility to pay back the outstanding amount gradually.

- Unforeseen Expenses: In the event of unexpected costs, cardholders (private or corporate) may require financial assistance. With the instalment feature, they can convert a larger purchase made on the credit card into instalments after the purchase, providing them with greater financial flexibility.

- Stock Replenishment for Businesses: Corporate cardholders who need to replenish their stock with a substantial purchase can benefit from the instalment feature. This allows them to finance the purchase over a specified period, ensuring a continuous supply of goods without straining their immediate cash flow.

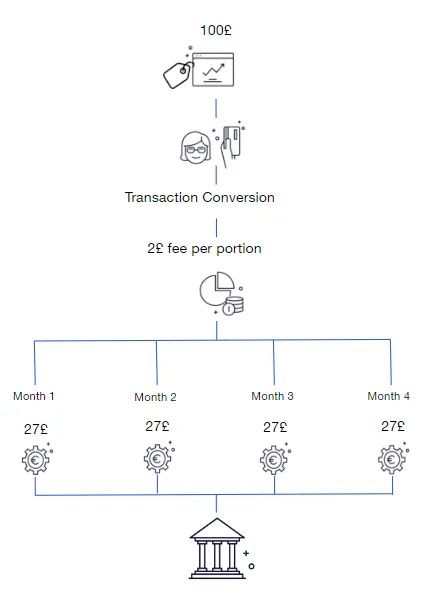

Converting transactions into instalments

With the instalments feature, credit card issuers can offer their customers flexible repayment plans through the ability to split specific retail or ATM transactions into instalments before invoicing. During the instalment plan setup, issuers have the flexibility to determine the following parameters:- Number of Instalment Periods: Choose the desired number of instalment periods based on customer preferences and financial needs.

- Instalment Portion Amount: Set the amount that customers will pay for each instalment, ensuring manageable and predictable payments.

Plan cancellation

If a plan is cancelled, the balance contained in the instalment plan is returned to the initial account. The balance that was previously contained in the instalment plan will be included in the revolving credit invoice cycle.

Portion threshold

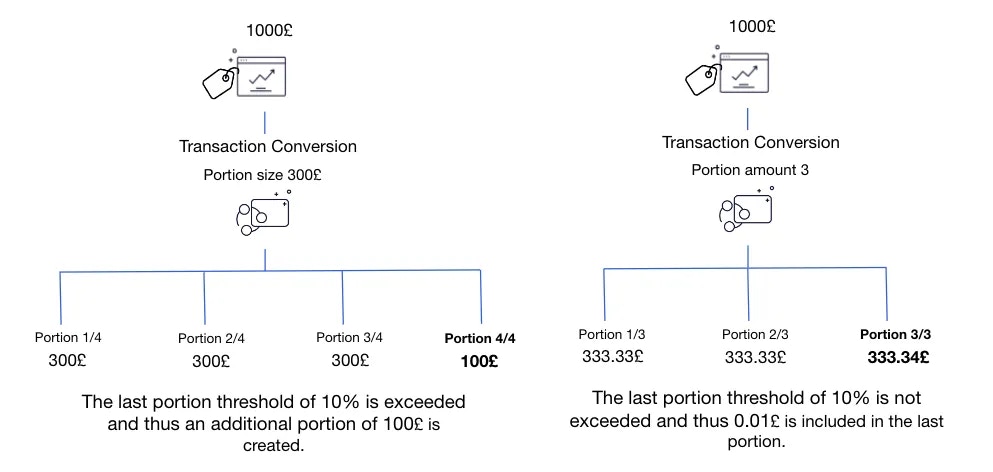

In order to avoid unreasonably small portions, a last portion threshold is configured. This threshold is based on prior portion size and can be set to an amount or a percentage. By default, the last portion threshold is set to 10%. This means that if the amount of the final portion is less than 10% of the amount of the previous portion, the amount is included into that portion. Below is an example of the last portion threshold when converting a 1000£ transaction.

Fees and interest

With Enfuce instalments, issuers have control over their fee structures and can choose from various options to suit their business requirements. The fees are included in the portion amounts to enable even payment amounts per month.Fee Options

- Plan and Portion Fee: Issuers can apply a flat fee for each individual instalment portion or plan. The fee can be a fixed amount per plan, a set percentage of the total transaction amount, or tied to the number of portions in the plan.

- Update Plan Fee: If customers request modifications to their existing instalment plans, issuers can implement a processing fee for plan changes.

- Closing Plan Fee: Issuers may opt to charge a fee when customers cancel their instalment plans prematurely.

- Late Payment Fee: Issuers can apply a flat fee for late payments.

Invoicing

Instalments are a part of the revolving credit product and applicable invoicing process. This means that instalment plans and portions are included in the monthly credit invoice files. A more thorough description of the invoicing process is available in the service description Revolving credit product – Invoicing process. The table below contains the additional instalment plan specific fields that are included in the invoice:Payments

Incoming payments will be credited to the account in the Enfuce system. The reason for incoming payments can be customers paying the invoice or increasing the balance or available amount on the account. For further information about payments in general please see customer payments. It is possible to choose the payment priorities to select which open balances will be covered first. In case of overpayment or other credits into the account, those will be posted as a credit on the account by default. It is also possible to change the account settings so that credit would cover the upcoming instalment balances. For the latter option please see more information from the incoming payments documentation.Instalment APIs

In summary, the following APIs are available for managing the instalment plans:- Create instalment

- Choose the retail or ATM transaction

- Choose how many portions or how big portions

- Get instalment

- Show instalment plans for the specific account

- Show portions for the specific instalment

- Get the transaction details for a specific instalment

- Get instalment details for a specific transaction

- Update instalment plans

- Change how many portions

- Close instalment

- Close instalment plan